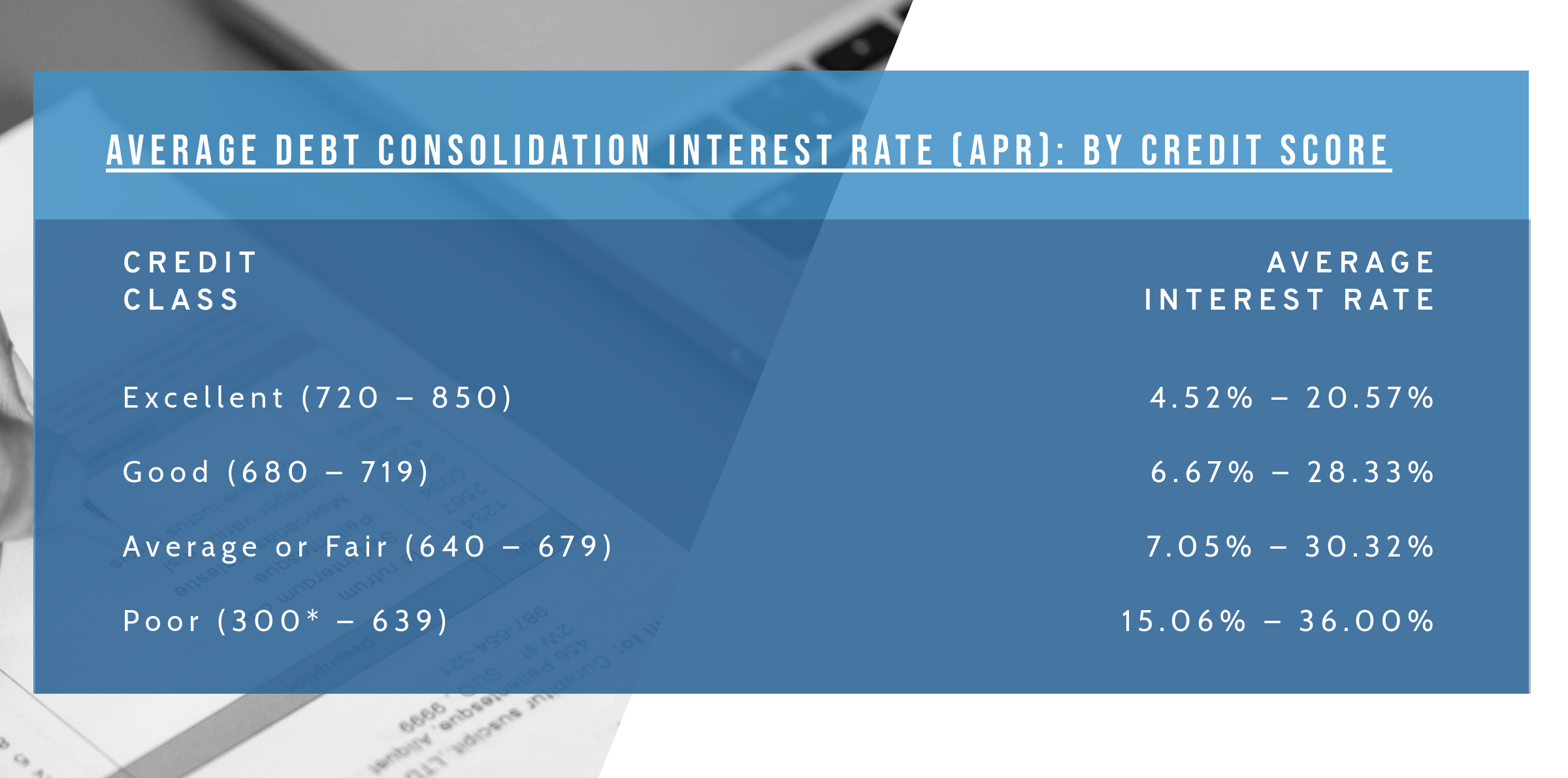

Occasionally, people who have most useful credit scores get shell out alot more during the costs, whenever you are those with straight down credit ratings pays quicker.

Washington — If you are searching to acquire a property, the newest federal laws can get perception how much you pay to own good financial.

Delivery Can get step one, initial costs to own funds supported by Fannie mae and you may Freddie Mac could be modified on account of changes in the mortgage Height Rates Adjustments (LLPAs). The individuals costs depend on one thing such as the borrower’s credit rating, size of the brand new downpayment, sorts of household and. Occasionally, individuals with ideal fico scores may shell out way more within the charges, whenever you are individuals with down fico scores will pay quicker.

Why is which happening?

The newest laws changes are part of brand new Government Housing Money Agency’s (FHFA) operate to include “equitable and you will sustainable access to homeownership” and also to bolster resource during the Freddie Mac computer and you may Fannie mae.

“Brand new [ Biden ] administration’s stated mission at the rear of and come up with such transform should be to help to make it more convenient for consumers who’ve usually become disadvantaged and possess got difficulty accessing borrowing from the bank,” Agent master economist Danielle Hale informed ABC News.

That would it perception?

The new guidelines just apply at fund supported by Fannie mae and you may Freddie Mac, and you can impact any the newest otherwise refinanced home loan signed May 1 otherwise later. According to Metropolitan Institute, Fannie Mae’s and Freddie Mac’s share of the mortgage markets along manufactured nearly 60% of all of the the fresh new mortgage loans in the pandemic when you look at the 2020. That is weighed against 42% for the 2019.

Homeowners whom set out a larger commission out of fifteen% so you’re able to 20% could see a larger rise in financial costs, but Bankrate mortgage expert Jeff Ostrowski asserted that must not changes an excellent borrower’s attitude.

“This new matrix individuals are seeking discover is just part of equation,” Ostrowski informed ABC Information. “One other region is financial insurance policies: Borrowers whom set lower than 20% down have to pay home loan insurance policies that more than offsets new down upfront commission. Therefore there’s no financial benefit to the brand new debtor to put off less than 20%.”

Just how will it performs?

“Brand new charges was quite more pricey for many borrowers having a good credit score, and you may a little cheaper for almost all consumers which have shorter-than-best borrowing,” Ostrowski told ABC Reports. When you yourself have an excellent credit history, you can however shell out lower than for those who have a deep failing one, nevertheless punishment for having a reduced credit score commonly today getting smaller compared to it had been may step one.

“From the transform, the benefit of having increased credit rating, or to make a more impressive deposit, is not as larger because used to be,” Hale said.

Eg, beginning May step 1, a buyer with a good credit score regarding 750 whom leaves off twenty-five% into an excellent $eight hundred,000 household carry out today spend 0.375% in the costs toward a thirty-year mortgage, or $step one,125, than the 0.250%, or https://paydayloanalabama.com/south-vinemont/ $750, in past percentage rules.

Meanwhile, a buyer that have a credit history out of 650 getting a 25% down-payment on an effective $eight hundred,000 home manage today shell out step one.5% inside the costs towards the a thirty-year loan, or $cuatro,five-hundred. One measures up having 2.75%, otherwise $8,250, within the previous rules.

With respect to the FHFA, the fresh new rules will redistribute fund to attenuate the interest rate paid down by the reduced accredited consumers.

So is this the great thing?

This will depend towards the person you ask. “It is a different sort of subsidy to try to purchase ballots,” previous House Depot Ceo Bob Nardelli informed ABC News.

The latest mortgage fee laws and regulations do-nothing to handle ongoing list pressures regarding the housing market, that is putting upward tension on home prices. The brand new median You.S. family rates when you look at the March is actually $400,528, with respect to the realty broker Redfin.

Specific construction professionals fear the fresh guidelines usually prompt banks in order to lend to help you consumers whom maybe shouldn’t be eligible for home financing during the the first put. Lending to help you unqualified people is really what lead to new financial crisis from 2008; financial institutions provided a lot of unqualified people lenders that they sooner or later didn’t pay-off.

“It confusing approach wouldn’t performs and you will, more importantly, decided not to been in the a worse time for an industry struggling to go back with the their base just after these types of prior 12 months,” David Stevens, a former commissioner of Federal Construction Government in the Obama administration, had written from inside the a social network blog post. “To take action at the start of the newest spring market is almost offending with the field, consumers and you may lenders.

Despite the alterations, Ostrowski mentioned that complete, mortgage charge always choose consumers that have good credit. “You still rating a far greater handle a robust borrowing from the bank rating,” he said. “The fee reductions don’t apply at consumers that have credit ratings from less than 680 — so tanking your credit score assured away from scoring a far greater contract do backfire.”

MOST COMMENTED

Tin Tức

Steeped Hands Gambling establishment No deposit Incentive Rules 25 100 percent free Chips!

mail in order bride definition

God’s elegance can do far to help you repair and you may heal the latest sexually broken and damaged

Tin Tức

Bally Wulff Fruit Mania Für nüsse zum besten geben exklusive Registration

Tin Tức

Mermaids Millions Slot Comment 2024 Winnings 7,500 mr bet blackjack online gold coins

Tin Tức

Cheats unter anderem Spieletipps: Diese drei besten Webseiten Die

Tin Tức

Fixed An excellent 90 best online casino ranked 0-kilogram ice hockey pro strikes an excellent 0.150-kg puck,

Tin Tức

hierher eintreffen